Skip to main content

Skip to main content

This interactive data graphic provides a brief description of how Washington’s budget-based property tax system works focusing on the State School Property Tax levy. The graphic includes:

- Market value compared to the statewide rate

- Statewide to county rate comparison

- Inflation history

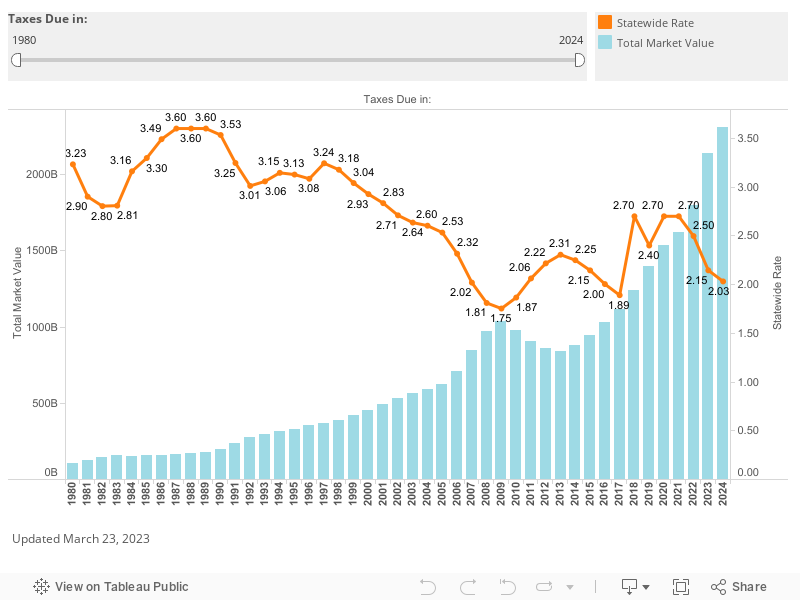

Market value of property compared to statewide rate:

All real and personal property in Washington is subject to property tax based on 100 percent of its true and fair market value unless the law provides a specific exemption.

The budget-based property tax system in Washington means that each taxing district determines the revenue needed to fund their budget and levies that amount within the confines of certain constraints. The county assessor calculates the levy rate by dividing the levy by the total value of the property in the taxing district. We express the levy rate in terms of a dollar rate per $1,000 of property value.

A budget-based system causes property tax rates to fluctuate based on the total value of the property in the district. For example, if property values increases faster than the levy amount the rate usually decreases. The chart below reflects the changes in statewide true and fair market value subject to the state levy and the statewide levy rate for the state property tax levy over time.

For property taxes due in 2018 through 2022, the Legislature established a total combined rate for both parts of the state property tax levy. This changes the state property tax from being budget-based to being rate-based for property taxes due between 2018 and 2022. After 2022, both parts of the state property tax levy will be budget-based.

Note: Data visualizations must be viewed in the Google Chrome, Firefox or Safari browsers.

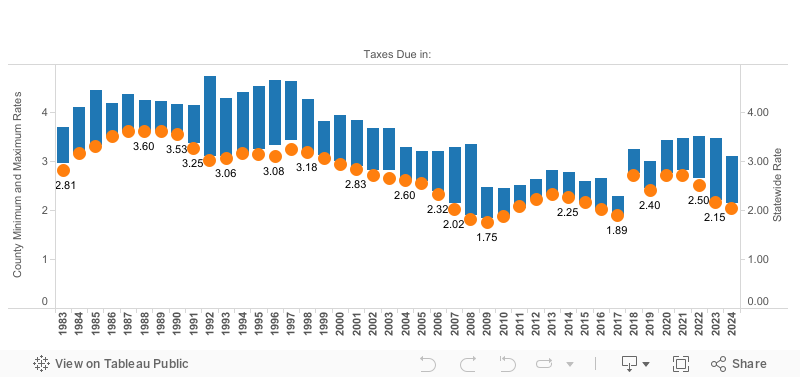

Statewide to county property tax rate comparison:

Taxpayers rarely see the statewide property tax rate based on 100 percent of true and fair market value on their property tax statement due to the difficulties assessors face when appraising property at 100 percent of true and fair market value. To keep the state property tax rate uniform across the entire state, county assessors calculate the state property tax rate for their county by dividing the county’s share of the state property tax levy by the total assessed value in the county subject to the state levy.

The following chart shows the variations across counties in the property tax rate taxpayers see on the tax bill compared to the statewide property tax rate.

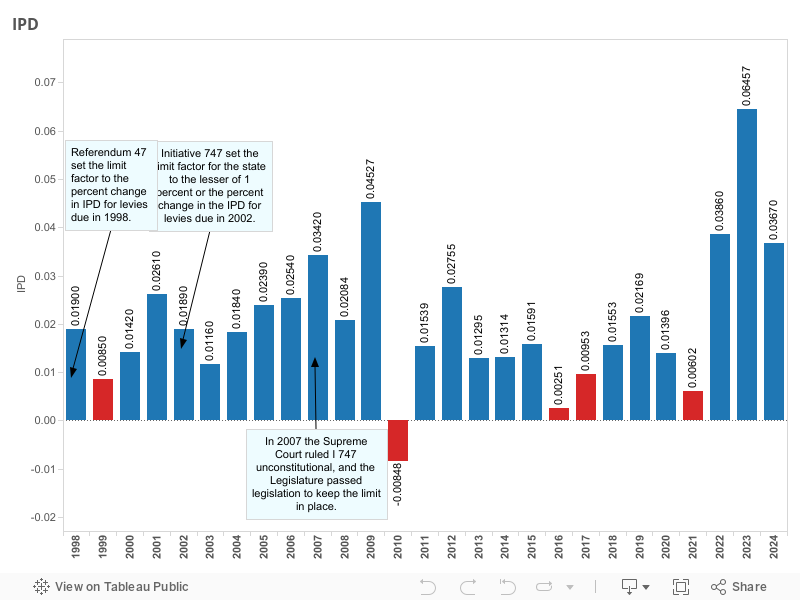

Inflation history:

Property tax levy limitations restrict or limit increases to property tax levies to inflation. One such limitation, started with Initiative 747, limits regular property tax levies in districts with a population of 10,000 or more to increase by the lesser of 1 percent or inflation. The law defines inflation as the percentage change in the implicit price deflator (IPD). For taxing districts with a population less than 10,000 the law limits regular property tax levies to an increase of 1 percent.

This chart shows the percentage change in the IPD since property taxes due in 1998. A red bar reflects a year where the percentage change was less than 1 percent.

Additional Information:

To learn more about Washington’s property taxes, the following publications provide additional information: